Why we removed the ability to connect your bank account to North and what we learned on the way

February 28, 2020 · 7 min read

After testing various implementations of integrating bank accounts into North, we’ve decided to remove the feature for now.

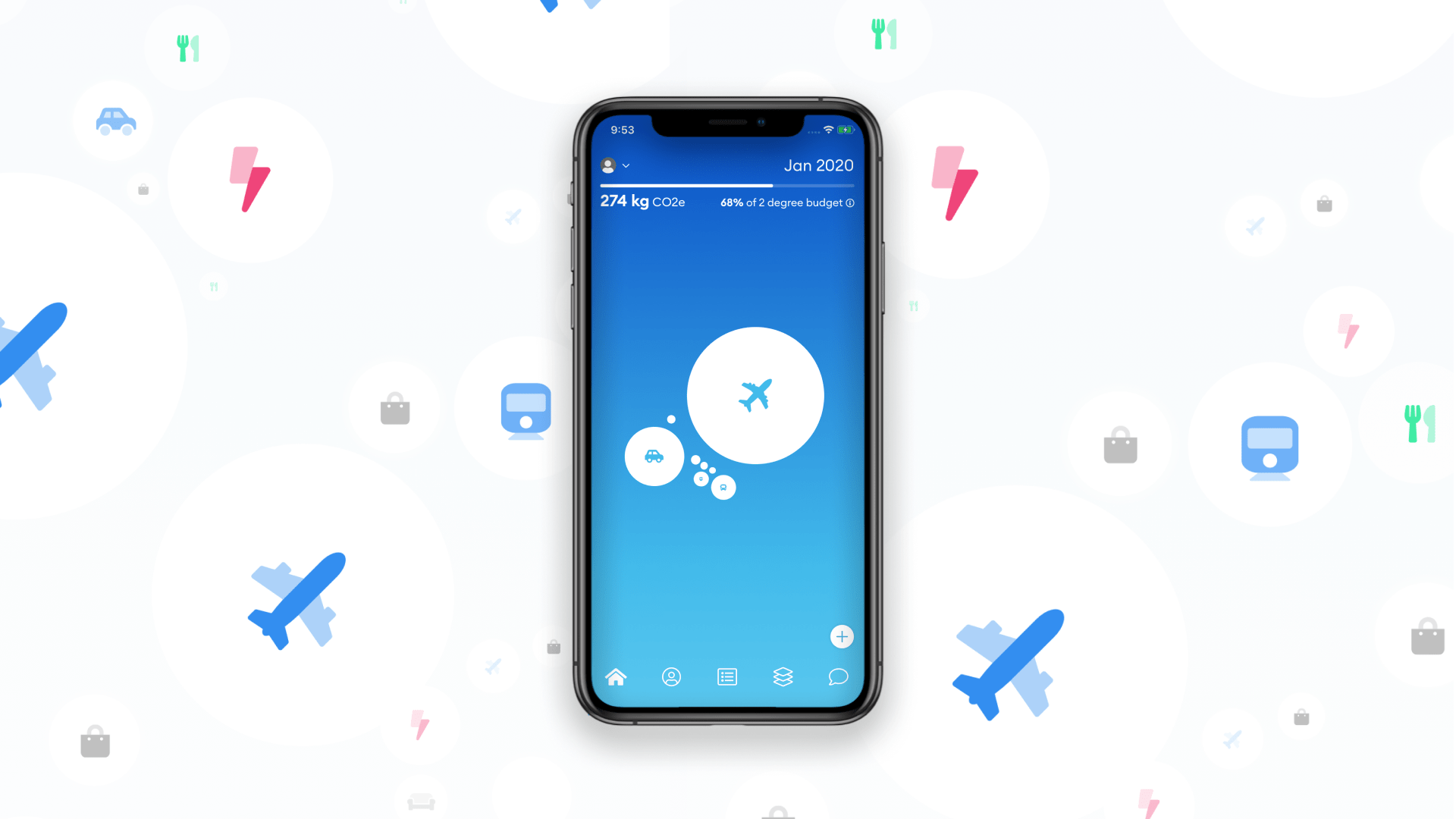

Such a feature would have allowed every user to automatically get the carbon footprint of their bank transactions in the North app. This is accomplished by matching bank transactions to categories linked to an input-output (which converts transactions to carbon footprint measurements) model for consumption.

While this sounds great, we found that the costs of this at our current stage were simply too high. We ultimately decided we could spend that money and time on other things that will have a larger impact. If you believe that conclusion is wrong after having read this article, please reach out to us at [email protected].

We hope this blog post can save like-minded climate entrepreneurs time and maybe inspire people to find better ways to do it.

If you want to read in more detail how we came to this decision: read along!

Why bank transactions are interesting

North’s core functionality is to connect to services and apps you already use to automatically let you track your carbon footprint. While in Denmark a lot of services are digital, this is not true for the vast majority of countries. Bank transactions, however, are the exception.

Recently, a lot of services have popped up allowing companies to get access (with a user’s permissions) to people’s bank accounts, mainly bolstered by recent EU legislation making the process a lot easier than it was before.

Simultaneously, input-output databases have become increasingly good at estimating what the climate impact of a purchase is. From research projects likeEXIOBASE to corporate solutions likeÅlands Index, these models allow banks to show all their customers a rough estimate of the climate impact of their consumption.

Indeed, for North, we saw it as a great opportunity to be relevant for users in many countries, as it would offer them an easy way to get an overview of their emissions in North.

How we built it

Here is how we went about creating the North banking integration:

- Connect to banks’ API (by ourselves or using an aggregator)

- Match a bank’s transaction category to an monetary carbon table (think X € in a category is equal to Y kg CO2eq)

- Show the climate footprint of the transactions in the North app

Of these three steps, the first, is the one that we found currently not to be a viable option - both working with an aggregator or getting a licence ourselves.

Partnering with aggregators

Some financial aggregators have an offering that allows users to give services (like North) the ability to access their bank transactions, removing the requirement for the third party (North) to have a license from a bank authority.

While we got very generous offers from bank account aggregators like Bridge, Tink and Nordic API Gateway (thank you so much!), it was difficult for us to come up with a financial model where we could make it work. Usually the contracts work with a fixed fee, and then a variable user fee per day or per month.

The main blocker here was that the user fee would be prohibitive at scale: we can’t afford to pay up to several euros per user per month. It is clear that financial aggregators’ business models are more geared towards Fintech companies with high revenue per user and/or few users and/or few requests.

To solve this issue, we even considered offering bank connection as a paid feature - essentially passing that cost on to willing users. However taking App store fees and VAT into account, users would have to pay even more than the direct cost per month. We believe that knowing your carbon footprint shouldn’t cost anything, and the cost we would have had to charge more than we expect users would be willing to pay.

Lastly, some of these services don’t offer yet transaction categorisation: it adds another layer of complexity as we would need to find a way to generate categories from limited information.

Getting a license ourselves

First, we considered not getting a license. After all, we do not store nor process our users’ data on our servers - we don’t have the user’s data anywhere. Ideally the way our integrations work is by letting the user’s mobile phone connect directly to the service without us being intermediaries. However, we quickly found out that this is not possible; banks are only required to give API access to someone with a certificate and thus an Account Information Services Provider (AISP) license.

For this reason, we also researched gettingan AISP license ourselves. What it would allow us to do was to use the PSD2 legislation and let our great community of contributors build the integrations themselves. We found several hurdles in this approach:

1) Costs

It would require us to spend between €10.000 and €20.000 in lawyer fees to get the license.We would also need to get a special insurance that would cost around 1.000€ per year, a IEDAS certificate that would also be around the same per year, and fees to the Financial Authority and Consumer Ombudsman that would be around 5.000€ per year. We would also expect to spend at least 7.000€ per year on lawyer fees to keep the license.

So an approximation of total costs - not including our own time - would be around 13.000€ per year on top of the 20.000€ upfront.

2) Administrative burden

A license granted by the Financial Conduct Authority is no joke - regardless of which European country you apply in. Your management and board need to be checked and ensure they’re ”fit-and-proper”. Complaints need to be registered, and governance is key to getting the license at all. For a small startup of 8 like us, speed is crucial. As we don’t see this as a core functionality of what we do, putting an extra burden on our shoulders did seem like a legitimate risk.

3) Technical challenges

Assuming we got a license, we would still have to work with plenty of different banks where transaction classification is definitely not the same everywhere, nor present all the time. We know from our talks with the aggregators that the bank APIs themselves are not always the most fun to work with - they have a tendency to not work very well, and it would require a lot of work from the community and us to ensure it was properly working.

Ce n’est qu’un au revoir

Clearly the reason why we’re currently not pursuing integration with banks is a resource (money and time) problem. It should be solvable. So we hope that while we crunch the other very important things, a light at the end of the bank transaction tunnel appears.

Here are ways we could see things change:

- Maybe one (or more) of the bank account aggregators will be interested in partnering up more closely, and work with us to make the climate impact of daily choices accessible to everyone.

- Some of the bank account aggregators with affordable pricing (for us) may add categorization to their services

- The PSD2 legislation and market is just getting started. There might be another, smarter way to solve this issue that doesn’t require a license in the future - or at least a cheaper one.

- We may be able to integrate directly with apps like Bankin’, Spiir or Mint which already have access to and categorize consumers’ bank transactions.

- One of our users may be Jeff Bezos who thinks some of his $10 billion grant would be well spent on making bank integrations free for all North users.

If you have a trick to fix any of the above things: reach out to [email protected] !

What does it mean for North today

- We’re removing the banking integrations we had thought we would integrate with

- We will keep the manual transactions input, on top of the other manual inputs and all the automatic integrations already in the app.

- We will focus on creating other integrations for now and then hopefully make banking integrations happen in the future!